Contents

1. What is a fixed asset?

2. How do fixed assets and inventory differ?

3. What are some fixed asset types?

3.1. Computer equipment

3.2. Furniture and fixtures

3.3. Machinery

3.4. Vehicles

4. What is fixed asset accounting?

5. International Financial Reporting Standards: An overview

6. What records does my fixed asset accounting require?

6.1. Procurement

6.2. Depreciation

6.3. Impairment

6.4. Disposal

6.5. Audits

7. Best practices for fixed asset accounting

7.1. Establish a threshold for capitalization

7.1. Ensure your assets have tags

7.2. Automate your insights

7.3. Choose the right depreciation method

7.4. Get insured and record it

8. Conclusion

1. What is a fixed asset?

Fixed assets are long-term tangible pieces of property. Companies use these assets in their daily business operations to generate an income. Often referred to as the ‘capital’ of the business, fixed assets include items such as machinery and plant equipment.

Their defining feature is that they are not converted into cash in the first year of acquisition. Firms tend to invest in fixed assets for the following objectives:

- Act as rentals for third parties

- Use them in regular organizational workflows

- Enable the production or supply of business goods and services

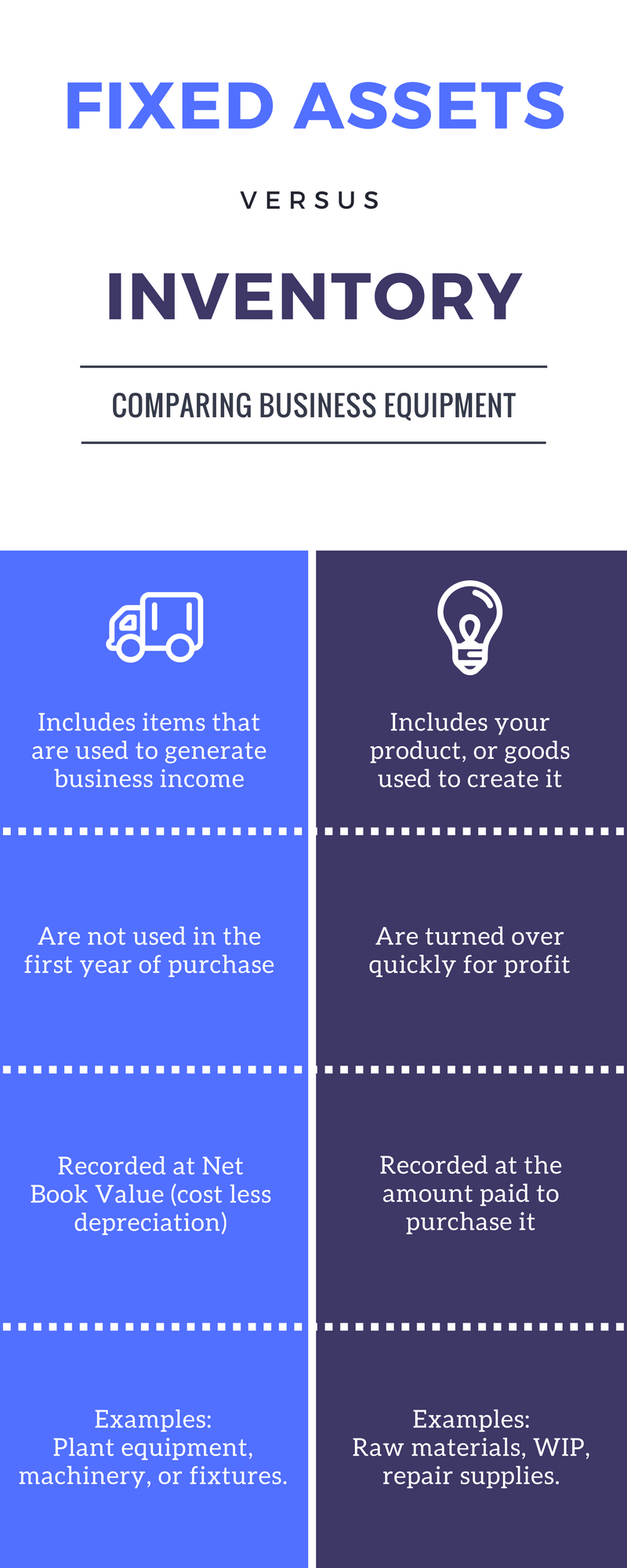

2. How do Fixed Assets and Inventory differ?

People often ask how fixed assets are different from inventory.

Business inventory is defined as any current asset in the financial database of your firm. Goods that fall under inventory signify the company’s worth. Moreover, a firm can easily cash them out to cover up any existing debts. For simplicity, we can divide inventory into four categories:

- Raw materials

- Goods and services in progress

- Finished goods

- Maintenance, repair and operating supplies

All of this greatly differs from what a fixed asset is. A fixed asset is, more often than not, a finite, long-term investment.

Another point to clarify here is that fixed assets don’t have to be ‘fixed’. This means that a fixed asset doesn’t necessarily have to be stationary or immobile. They can be easily moved around from one location to another. Good examples include vehicles and computer equipment.

The best way to dispose of a fixed asset is to sell it at its salvage value. Different companies may calculate salvage values differently but it usually depends on the frequency of use, item type, and deprecation rate.

The procurement patterns for these assets tend to be quite costly and have high lead times. However, if you manage to keep accurate records for your fixed assets, this helps you in many ways.

For starters, it enables you to build the company’s credibility for any future loan opportunities. Furthermore, it also pushes you to make the most out of your business investments.

3. What are some fixed asset types?

Any firm’s primary objective is earning profits – no surprise there. To ensure this, firms invest in a few common types of fixed assets. Without these, your organization may struggle functioning at optimal levels.

Here are some examples of the fixed assets that every business owns:

3.1. Computer equipment

In the current technological world, accomplishing any task without the use of computers is challenging. This is why almost all your employees in every department have a personal machine to work on.

More than 40% of workers spend a quarter of their workweek doing manual, repetitive tasks. Computers enable you to automate these and help you track task progress in a more systematic way. They also help streamline company correspondence so collaboration is never a problem.

3.2. Furniture and fixtures

Every office building is stocked with furniture and fixtures. These can either be movable items, such as desks, or utilities affixed to buildings, such as lights.

These types of fixed assets play a fundamental role in ensuring the smooth working of day-to-day tasks. While these may be items you don’t note of during the day, but they will cause a great deal of disruption when they break down.

3.3. Machinery

The type of machinery a company uses depends on its particular industry. For example, a construction firm most likely has numerous trailers and cranes. Furthermore, tools and instruments facilitate technical work and help achieve operational efficiency.

To maintain this, companies need to keep their machinery in good shape. For that to happen, they must implement robust maintenance sessions regularly.

3.4. Vehicles

There are now more business operations that require frequent travel than before. To tend to these, companies allocate separate budgets for specific vehicles.

For firms working on off-site projects, large trucks are a good choice. However, for shorter routes, smaller cars make more sense and are cost-effective too.

4. What is fixed asset accounting?

Fixed asset accounting relates to the accurate logging of financial data regarding fixed assets. For this purpose, companies require details on a fixed asset’s procurement, depreciation, audits, disposal, and more.

Since fixed assets form a substantial part of a company’s investments, it is imperative to record its specifications correctly. As per financial processes, fixed assets are listed under cash flow statements. This is why a purchased fixed asset is a cash inflow, while one that is sold is a cash outflow.

Next comes the question about how fixed assets are valued. Due to their continuous usage, fixed assets are subject to constant devaluation. As a result, these assets decline in value each year. A fixed asset, therefore, appears in accounting books at its net value. The net value is its original cost depreciated according to a specific rate over the years.

When you are first adding a fixed asset to your financial records, you need to carry out the following transactions:

- Periodic depreciation (applicable to tangible assets)

- Amortization (applicable to intangible assets)

- Disposal

Read More: How can I Calculate and Track Depreciation?

Keep in mind that, for reliable accounting procedures, it is always best to calculate specific depreciation rates for all your fixed assets. Once the asset’s value entirely depreciates and it completes its useful life, the last step is its disposal. Recording disposal is as important as entering data about a new purchase.

Now that we know what fixed asset accounting is, let’s take a look at ensuring the smooth functioning of your fixed asset accounts.

5. International financial reporting standards: An overview

For fixed asset accounting, the International Financial Reporting Standards (IFRS) is a framework that provides uniform guidelines to prepare and organize financial data. Actively endorsed by more than 120 countries, the IFRS has been derived from the International Accounting Standards Board based in London. Why does all of this matter to your company’s fixed asset accounts?

Companies across the world are likely to have different asset management structures. This means they will also have different methods to document asset usage. To bring some consistency among such variations, the IRFS has set forth rules and regulations for countries to follow.

If your company lacks robust accounting processes, it is likely to suffer in the long run. For this reason, the IFRS encourages companies to acquire a set of authorized accounting directives. These help manage errors, negligence, and fraudulent activities.

Using these standards allows organizations to design and execute sophisticated management strategies for various processes such as:

- Documentation of financial records

- Revenue calculation

- Employee welfare practices

- Fixed asset valuation

- Income tax regulation compliance

Therefore, choosing a universally accepted mechanism, such as the IRFS, works in favor of all companies. It makes it easier to report statistics without having to undergo costly conversions. If you want to compete within international markets, it is best to opt for a financial structure that allows you to do so easily.

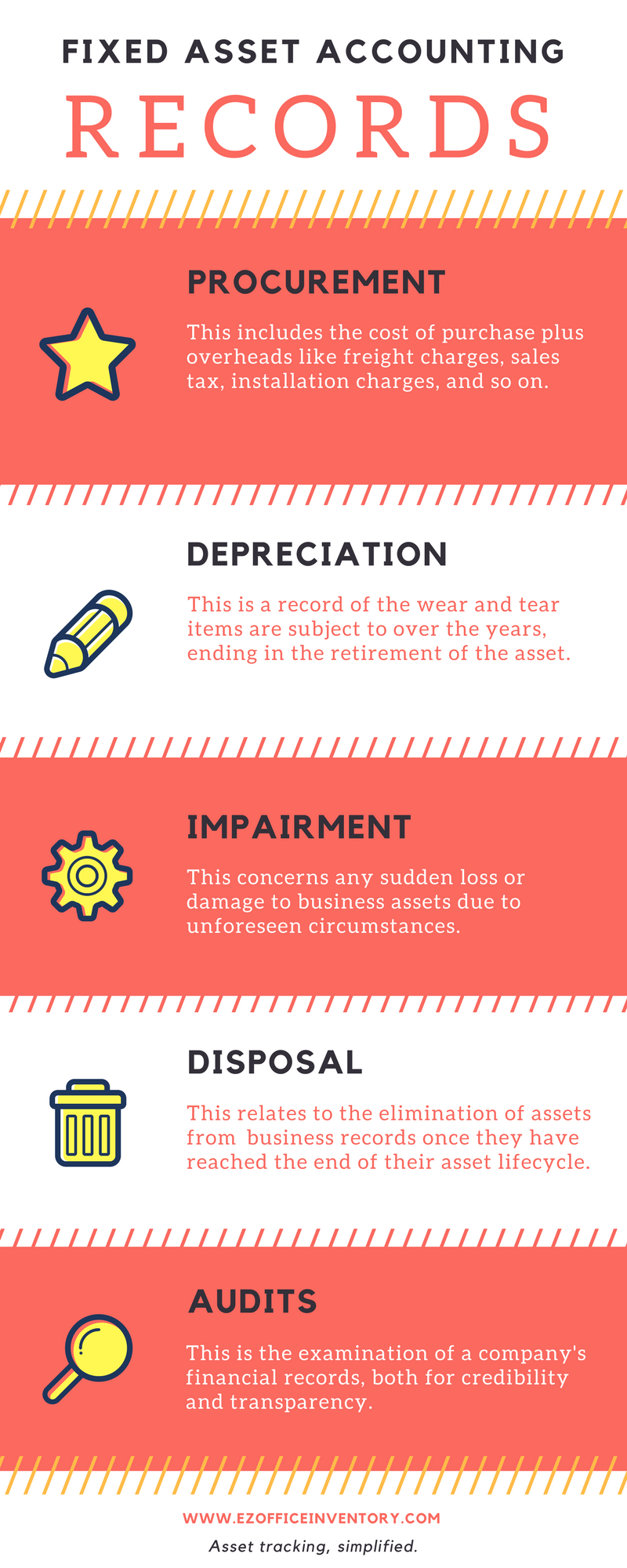

6. Which records does my fixed asset accounting require?

As soon as you acquire a new asset, you should add certain details to your financial reports as well. Doing this lets you maintain an up-to-date database, from purchase to disposal, so it’s easy to determine the exact worth of all your assets.

Here are the key processes that need to be documented.

6.1. Procurement

This refers to the initial acquisition of any type of fixed asset. For convenience purposes, we assume that your company is obtaining assets on credit. Following simple accounting methods, the first entry is a credit entry under the account payable section.

Along with this, there is a debit entry to the specific fixed asset account. The debit entry equals the cost of the asset. This cost can also include any other overheads incurred, including freight charges, sales tax, installation charges, and so on. You can generate several fixed asset accounts to accommodate equipment, machinery, land, and vehicles.

6.2. Depreciation

All tools or machines undergo wear and tear over time. This process is called depreciation. You need to monitor depreciation in your financial records as well. The journal entry for devaluation can be a single one or divided into different sections, depending on the number of fixed assets.

You record this entry as a credit to the accumulated depreciation account and a debit to the depreciation expense account.

Over the years, the accumulated depreciation balance continues to increase in value until it equals the total cost of the fixed asset. At this stage, you can stop accounting for depreciation and formally retire the asset.

6.3. Impairment

The next stage in fixed asset accounting is to assess the impairment loss to your equipment. Impairment usually concerns any sudden loss or damage to the assets due to unexpected circumstances. If your company assets undergo impairment, then you have to document this change in the financial statements as well.

To calculate impairment loss, it is important to know these terms:

- Carrying amount: This is the total cost of the asset without the addition of its accumulated depreciation.

- Recoverable amount: This amount is the maximum benefit a company can obtain from an asset. It is equal to the greater of the two – fair value minus costs to sell, or value in use.

- Fair value minus costs to sell: This is the amount obtainable from the sale of the asset. It is the difference between the current market value and the costs of disposal.

- Value in use: This is the amount of the present value for cash inflows that the asset derives under a specific use.

Once you receive the carrying amount, you have to compare it with the recoverable amount. If the carrying amount is greater than the recoverable amount, you can credit the accumulated impairment and debit the impairment loss.

6.4. Disposal

As soon as an asset completes its life cycle, you have to remove it from your financial documents.

This process involves reversing the accumulated depreciation and fixed cost accounts. If the asset has fully depreciated, then credit the fixed asset and debit all accumulated depreciation.

However, there could have been some sort of gain or loss from the sale of the asset. In such a situation, the company has to recognize that as well.

6.5. Audits

An audit is the examination of company financials.

There are many reasons why audits are important. For starters, companies carry out this activity to establish credibility and reliability within the market. Another reason is to promote transparency within the company itself.

Even when it comes to fixed asset accounting, audits have several benefits. They allow companies to supervise usage patterns and stop any unauthorized practices. To carry out fixed asset auditing, auditors tend to observe or recalculate the following business records:

- Purchase and disposal authorizations

- Lease documentation

- Appraisal reports

- Accumulated depreciation or amortization amounts

Audits inspect the accuracy of financial reports and try to validate all business transactions. Depreciation discount rates also pass through a valuation test to ensure that correct processes were followed. Lastly, audits examine the classification of fixed assets as well.

7. Best practices for fixed asset accounting

Asset accounting is a crucial task for firms. Therefore, all firms need to ensure that they carry out the process with utmost care. A single error in financial reports can lead to grave consequences – potentially damaging company integrity.

Read More: Five Tips for a Fixed Asset Manager

The best way to go about this is by observing the following best practices.

7.1. Establish a threshold for capitalization

The first step towards maintaining error-free accounts involves setting a criterion to distinguish assets from expense items. Experts recommend recording items that are to be used for more than a year as assets. Doing so is handy as it also helps you differentiate between different accounts. Moreover, it also saves you from material misstatement in your financial reports.

7.2. Ensure your assets have tags

Many companies have fixed assets that they transport to various locations for off-site projects. However, all this movement might make it difficult to track the assets.

With the inability to track assets comes the consequence of facing huge losses from theft or misplacement.

In order to control such unfavorable activities, it is critical to tag all assets. Barcode and QR Code labels are a good option for easy check-ins and checkouts. These tags let you supervise asset whereabouts at various locations.

With this information, you have more accurate data for your financial reports as well.

7.3. Automate your insights

These days, a huge number of companies resort to cloud based fixed asset tracking software for tracking assets while also carrying out fixed asset accounting efficiently.

Such software offers a variety of features, such as tracking asset usage from the time of purchase to disposal. Real-time electronic records such as the one aforementioned help reduce human error. This lets you maintain an accurate database that you can then update from anywhere, and at any time.

7.4. Choose the right depreciation method

Most companies fail to come up with the correct depreciation rate for their assets owing to unreliable methods of calculation. If a company continues to apply the incorrect rate, their data will be full of errors.

To avoid such scenarios, classify your assets according to their use, durability, and expected life. Then, determine the best possible depreciation method on the basis of the unique attributes of these distinct groups. What works for a group of laptops, for example, won’t necessarily be the best option for heavy plant equipment as well.

7.5. Get insured and record it

Since fixed assets are used for over a year, it is a good idea to get them insured. Insurance coverage allows you to tackle unexpected damages to your assets without emptying your bank account.

Make sure you record insurance claims against their respective accounts. This includes properly stating the damage and its compensation details. You’ll find this beneficial later on as it helps provide the true representation of asset usage to build the firm’s credibility.

8. Conclusion

Fixed asset accounting is an intricate process that requires a lot of attention to detail. In order to maintain precise financial reports, firms need to oversee all work processes regarding fixed asset usage.

Moreover, they must be diligent when capturing important data relating to these assets. Success in maintaining reliable accounting reports can help firms exercise robust preventative maintenance, improve productivity, and deter theft.

About EZOfficeInventory

EZOfficeInventory is a leading asset tracking software. It allows you to track, maintain, and report on inventory from anywhere, at any time.